Client Care

/client-care/make-a-claim/submission/

/client-care/client-charter/

/client-care/make-a-payment/overview/

/client-care/client-charter/

/client-care/make-a-service-request/insurance/

/client-care/client-charter/

https://sunaccess.sunlifemalaysia.com/portal-ui/eDocumentSubmission

/client-care/client-charter/

/client-care/frequently-asked-questions/services-tax/

/client-care/client-charter/

/client-care/fraud-and-cybersecurity-awareness/overview/

/client-care/client-charter/

/client-care/downloads/

/client-care/client-charter/

/client-care/client-charter/overview/

/client-care/client-charter/

/client-care/treat-clients-fairly-charter/overview/

/client-care/client-charter/

Client Charter

| Pillar 1 | INSURANCE / TAKAFUL MADE ACCESSIBLE |

|---|---|

| Description |

|

| Expected Outcome | BETTER ENGAGEMENT & IMPROVED SERVICES |

| Service Level Target |

|

We will make insurance and takaful products easily accessible via various channels, physically and virtually, to obtain information, purchase, or make enquiries.

To this end, the following are to be adopted:

- Offer an active engagement model wherein a client is aware of:

- Multi-channel options and accessibility for making purchases and enquiries.

- Where and how to provide feedback, suggestions and complaints.

- Reinforce that insurance / takaful is easily accessible via various channels, physically and virtually.

- Clients are kept informed on the physical and engagement channels available for them to purchase products or to make enquiries.

- Specifically, clients should have access to the following:

- An insurance / takaful agent locator.

- List of client engagement channels, i.e. corporate website, self-service client web portal and call centre.

- Social media (if applicable)

- Channel availability may vary from time to time, and clients will be informed accordingly.

- We are dedicated to making our insurance and takaful products accessible to all consumers. We strive to remove barriers and provide multiple access channels, ensuring everyone can secure the protection they need.

We will actively seek feedback, suggestions, or complaints on how insurers can serve clients better.

1. Clients are provided with available channels to provide feedback and suggestions via:

- Corporate website: www.sunlifemalaysia.com

- Self-service client web portal: https://sunaccess.sunlifemalaysia.com

- Call Centre: 1300-88-5055

- Branch: Sun Life Malaysia Assurance Berhad / Sun Life Malaysia Takaful Berhad 338 Jalan Tuanku Abdul Rahman, 50100 Kuala Lumpur

- Email (General Enquiry): wecare@sunlifemalaysia.com

- Email (Complaint): clientresolution@sunlifemalaysia.com

- Fax: 603-2614 3550

- Mailing Address: Level 11, 338 Jalan Tuanku Abdul Rahman, 50100 Kuala Lumpur, Malaysia

- Social Media: facebook.com/SunLifeMalaysia or instagram.com/sunlifemalaysia_my or youtube.com/user/SunLifeMalaysia.com.

| Pillar 2 | KNOW YOUR CLIENTS |

|---|---|

| Description |

|

| Expected Outcome | BUILD TRUST |

| Service Level Target |

|

We will strive to help clients find the right product to suit their needs.

- Knowledgeable and ethical staff and agents are available to serve clients.

- Training:

- Ensure employees and intermediaries are properly trained on products and services offered.

- Training must be provided any time a new product is launched and regularly as refresher courses on existing products.

- Understanding Clients’ Needs.

- In order to understand the clients’ profile adequately, insurers and takaful operators including their agents shall:

- Listen attentively to the clients.

- Acknowledge and properly understand the clients’ needs and preferences.

- Ask for requisite information and documents to advise the clients accordingly and in accordance with the Industry’s Code of Practice on the Personal Data Protection Act 2010.

- Offer options of suitable products and services to meet the clients’ needs and wants.

- We ensure all product information is communicated clearly and presented in plain language to facilitate clients’ understanding of the key product features, risks, and their rights and responsibilities .

- Any options provided to clients shall be explained and on an “opt-in-basis”, e.g. riders, sharing/using client information for marketing and research purposes.

Note: Handling of client information is governed by Bank Negara Malaysia’s Policy Document on Management of Client Information and Permitted Disclosures and insurers/takaful operators shall operate accordingly.

| Pillar 3 | TIMELY, TRANSPARENT & EFFICIENT SERVICE |

|---|---|

| Description |

|

- 80% of clients are being served within the expected service level and timelines.

- 100% of clients are issued with policy documents in a timely manner.

- Declining complaints ratio.

We will set clear responsibilities towards clients and uphold it.

We are committed to delivering service that is timely, transparent, and efficient. We ensure all communications are clear, accessible, and provided in various formats to meet diverse needs. A standard commitment on clear responsibilities to be a mandatory write up on all client charters should cover the following guiding principles:

- A clear and concise objective of the Charter.

- Mission

- Values to be provided to the client, e.g. fairness, transparency, integrity, ethics, professionalism, timeliness.

- Efficient/Effective communication channels.

We will set clear expectation on time taken for various services.

To include a clear expectation on time taken for various services:-

- Delivery of Services:-

- Information on turnaround time on delivery of services must be made available in the Clients Charter through various channels. (head offices/branches/brochures/call center/website/social media).

- Standards to be adopted:-

Serve Walk-in Client Promptly:- Client Waiting Time: Within 10 minutes.

We will ensure efficient policy servicing and providing relevant documentation in a timely manner.

- Clients shall be informed of each step and documentation required to alter, renew, surrender or cancel a policy, e.g. what happens when there are changes to the policy, notice on renewal, etc. as well as consequence arising from any of these actions.

- Clients are to be reminded in the renewal notice to inform the insurance company of any changes in the risk before renewal.

- The standard operating procedure on dealings with clients must be clearly complied with.

- We adhere to ethical practices in all interactions, ensuring that no client is subject to exploitation or unfair treatment.

- Policy Account Turnaround Time (from receipt of full documentation, information and payment of premium):

- Policy Issuance (upon acceptance in the policy system) New and Existing Client:-

- Standard cases - within 5 working days

- Additional information required/pre-existing medical condition/complex cases - within 10 working days

- Change of policy account details (endorsement):

- Policy Changes (Non-financial) : within 3 working days

- Policy Changes (Financial) :

- Standard cases - within 5 working days

- Non-Standard cases - within 10 working days

- Reinstatement: within 10 working days (with payment & complete documentation.)

- Renewal notice issuance:

- For policy with guaranteed renewal, premium due notice will be issued not less than 30 calendar days before the next premium due date.

- Notification of Revised Premium to renewable basic term policy/term rider will be issued not less than 30 calendar days before the expiry of existing policy/rider.

- Cancellation/surrendering of policy: 10 working days upon receipt of full documents - to also include processing of refund premium.

- Issuance of medical/hospitalization card for individuals - Within same business day of policy issuance.

Note: The timelines above do not take into account onboarding process - insurers/takaful operators have their own onboarding process/introduction to its products and services.

We will ensure efficient policy servicing and provide relevant documentation in a timely manner (General)

- Life Insurance - within 10 working days (applicable for individuals only, not applicable to group)

- Change of policy details/reissuance upon lapse/endorsement (upon acceptance in the policy system):

- Life Insurance - within 5 working days

- Renewal notice issuance: 30 calendar days before expiry of existing policy.

- Cancellation/surrendering of policy (including refund of premium).

- Non-Motor - within 7 working days

Note: The timelines above do not take into account onboarding process - insurers/takaful operators have their own onboarding process/introduction to its products and services.

We will be open and transparent in our dealings

The following information shall be easily accessible and made available through the various channels of communication such as branches/brochures/call centers/website:

- Product related details, i.e. product features, product disclosure sheets, terms and conditions, key facts and exclusions will be shared at the point of sale.

- Fees, charges (other than premiums), and interest (if any) as well as obligations in the use of a product or service (e.g. when premium needs to be paid and explaining payment before cover warranty).

- Anti-fraud statement and key points to remember, i.e. confidentiality of client information, free look period of not less than 15 calendar days to reject or accept applications.

- All the above information shall be explained and stated using simple words and in an easy to understand manner.

An enquiry refers to a request for information that does not allege dissatisfaction or financial detriment.

A complaint refers to any expression of dissatisfaction relating to products, services, decisions, or conduct that requires investigation, resolution, or remedial action.

- Phone.

- Where no follow up is required, we aim to resolve the matter immediately (first call resolution).

- Where follow-up is required, we will respond within 3 working days from the date of the first call.

- Written (Email, fax, written letter & social media).

- For Email/Social media:

- For complaints, an acknowledgement will be provided by the next calendar day, confirming receipt and expected resolution timeline.

- Non-complex enquiries will be responded to within 3 working days from the date of receipt.

- For letter or fax

- Non-complex enquiries will be replied to within 3 working days from the date of receipt.

- For complaints, an acknowledgement will be provided no later than the next calendar day.

- Counter/Branches.

- Where no follow-up is required, we will endeavor to provide first touch point resolution immediately.

- Where follow-up is required, we will respond within 5 working days from the date of the first visit.

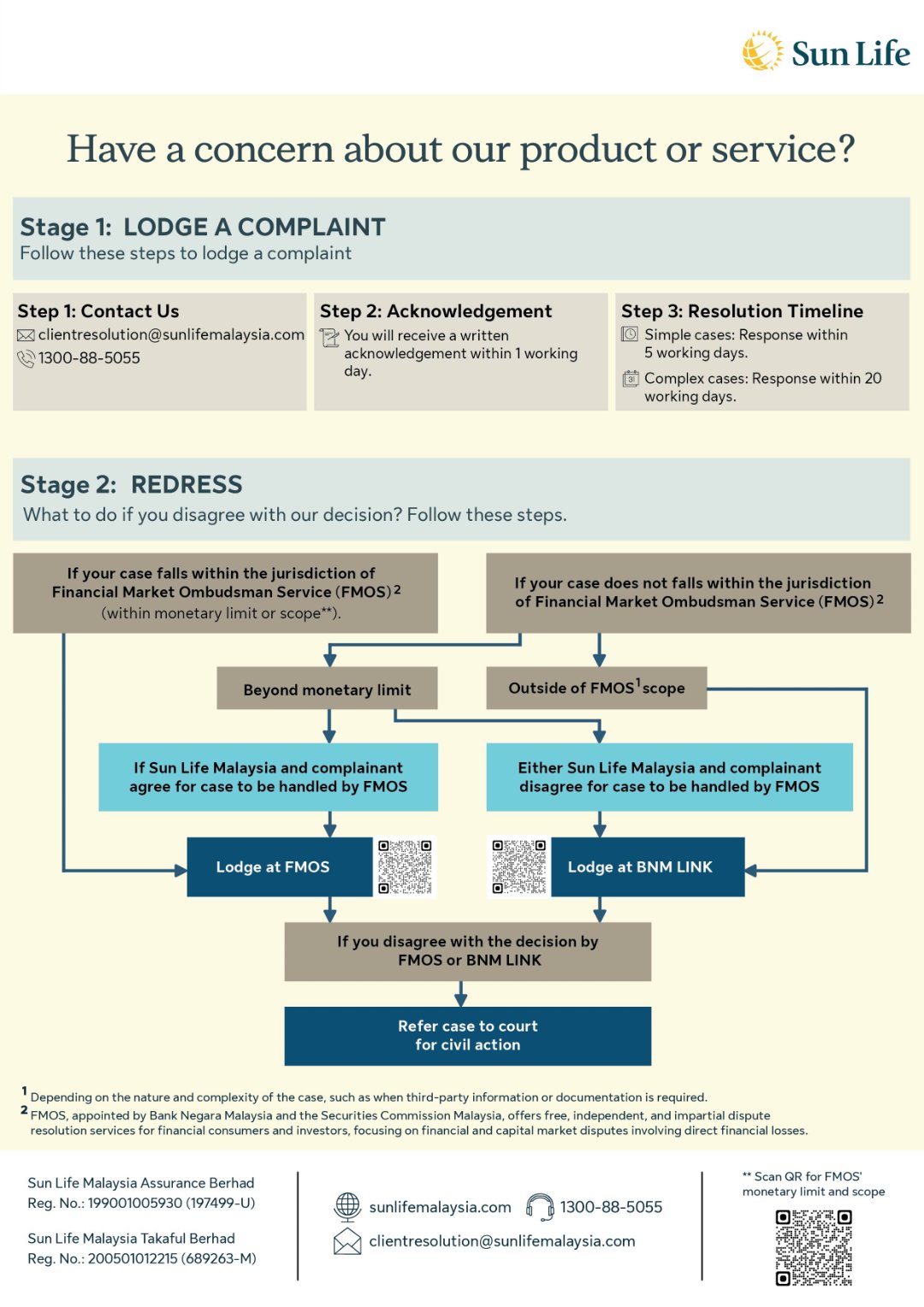

We will ensure consistent, fair, and thorough complaints handling.

We are committed to providing accessible, compassionate, and efficient mechanisms for all clients, including those in vulnerable circumstances, to lodge complaints.

- Clients or their authorized representatives shall be informed of the various options for submitting a complaint through available channels, including our complaints unit contact details, website, and social media platforms, where applicable.

- A verification process has to be performed on the policyholders/participants.

- Communicate clearly on the issue and gather adequate information for an informed resolution.

- Address the issue in an equitable, objective and timely manner, and communicate the decision and reasons clearly to the complainant. For simple complaints, we shall inform complainants of the decision within 5 working days from receipt. For complex complaints, we shall inform complainants of the decision no later than 20 working days from receipt.

- Where a complaint requires further investigation, insurers/takaful operators shall inform the complainant accordingly and provide periodic updates at reasonable intervals until resolution.

- Keep complainants updated with reasons and revised timelines if the complaint cannot be resolved within the stipulated timeframe.

- Where complainants remain dissatisfied with our decision, they shall be informed of their right to escalate the matter to Bank Negara Malaysia (BNMLINK) or the Ombudsman for Financial Services (OFS), including applicable jurisdiction and contact details.

Note: Complaints handling processes and timelines are governed by Bank Negara Malaysia’s Policy Document on Complaints Handling.

| Pillar 4 | FAIR, TIMELY & TRANSPARENT CLAIMS SETTLEMENT PROCESS |

|---|---|

| Description |

|

| Expected Outcome | PROVIDE PEACE OF MIND TO CLIENTS |

| Service Level Target |

|

We will set clear timeline for claims settlement process and strive to settle claims within these prescribed timelines and in a transparent manner. We pledge to handle all claims fairly and promptly. We have dedicated support mechanisms in place to assist consumers throughout the claims process, ensuring a smooth and straightforward experience.

To set clear timeline for claims settlement process and strive to settle claims within these prescribed timelines and in a transparent manner by adopting the following procedures:-

- Clients will be informed of the estimated time taken for claims settlement process and expected service standard. This information shall be made available through various channels (i.e. branches/brochures/call centers/website).

- Clients shall be informed on the acknowledgment of their claim within 7 working days from receipt of claims notification.

- All claims notifications through agents must reach the insurers within 3 working days, except for crime related claims which should be notified within 24 hours from time of loss.

- If documentation/information is incomplete, clients shall be informed within 14 working days from acknowledgement of the claim by the Claims Department.

- To state key claims procedures and assign timelines to it, i.e. appointment of adjuster, claims assessment, etc.

- Clients will be updated on the progress/decision every 14 working days.

- In the event of a catastrophe/disaster, e.g. large number of claims may be received, as such meeting timelines stipulated may not be possible, the insurers will strive to update every 20 working days on the progress.

To keep the client informed of the next level of escalation if the claims settlement/repudiation is not to his/her satisfaction.

- Clients shall be provided with available channels to appeal on a decision/raise disputes. (i.e. branch/brochures/call center/website).

- Any letter of rejection/repudiation of any element of a claim and dispute on quantum which is within the purview of the Financial Ombudsman Scheme must contain the following statement prominently:-

If you are not satisfied with our response or decision, and if your complaint involves a sum of up to RM250,000, you may lodge your dispute to the Ombudsman for Financial Services (OFS), within 6 months from the date of our final decision at the following address:

Financial Market Ombudsman Service (FMOS)

(Formerly known as Ombudsman for Financial Services)

Level 14, Main Block, Menara Takaful Malaysia

No. 4 Jalan Sultan Sulaiman

50000 Kuala Lumpur

Tel: +603 2272 2811

Fax: +603 2272 1577

Email: enquiry@ofs.org.my

Link: http://www.ofs.org.my/en/feedback.html

Website: www.ofs.org.my

Link: http://www.ofs.org.my/en/

Or

If your complaint does not fall within the purview of the OFS or for claims amount above RM250,000, you may refer your complaint to BNMLINK at the following address:

Bank Negara Malaysia

Pengarah

Jabatan LINK & Pejabat Wilayah BNM

4th Floor, Podium Bangunan AICB

No. 10, Jalan Dato’ Onn

50480 Kuala Lumpur

Tel: 1-300-88-5465

BNMLINK Webpage: bnm.gov.my/BNMLINK

Note: for the policy owners who made a claim/report involving claims settlement/rejection which is not to his/her satisfaction